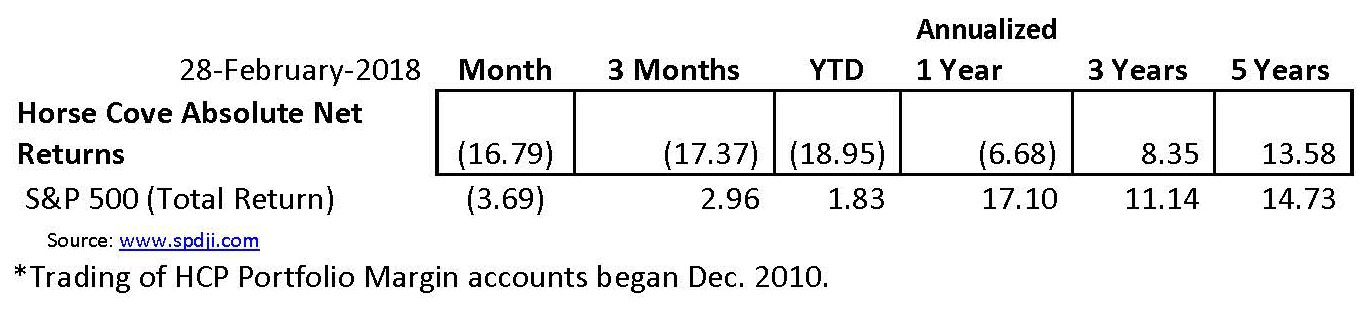

The February 28, 2018, month-end performance estimate for the Horse Cove Partners Absolute Return Strategy is -16.79% net of fees1. Since the December 2010 inception of trading, the Strategy has achieved a total cumulative return of +258.39%.

Total assets under management as of February 28, 2018 - $124.7 million.

Market Recap and Commentary

S&P 500 Total Return for the month of January was down -3.69%.

The short volatility trade finally blew up February 5, 2018, and with it, VIX spiked +116%. It was the largest single-day move in the VIX since its inception in 1990. What was a large spike in volatility was compounded by the record number of investors short the index, a winning trade for most of 2017. Short covering drove VIX over 50 and forced the liquidation of at least one ETF, which was a total loss for its investors. If there is good news, it’s that the money from those funds is no longer putting artificial downward pressure on VIX, and we should see the VIX Index behaving in a more historically consistent manner. We would hope and expect, to see the VIX continue through the rest of the year, as that tends to be favorable to our strategy.

The first half of February gave us the 3%, 5% and 10% corrections, for which the S&P 500 seemed long overdue. Cooler heads prevailed in the end, and the market spent most of the rest of February trying to recover its losses. The SEC and other regulators have begun looking into further regulation on the heavily leveraged long and short volatility products, as well as the type of investors for whom those products are appropriate. Business and the economy are still strong. While the market and economy appear to be in the same place they were in early January, the major difference is that investors have become aware that this bull market has gone on a long time and that there are risks (as we have mentioned once or twice before).

Performance and Trading Update

The Horse Cove Partners Absolute Return Strategy composite was down (16.79%) net of fees in February.

A large spike in volatility is very difficult for the strategy and February was no exception. We have now seen three of these spikes since we began actively trading: the fall of 2011, August of 2015 and now February 2018. We have not been able to predict them and when they come, we maintain our discipline and take defensive action to limit the potential for large losses.

On January 26, 2018, the day the stock market hit its high, the VIX closed at 11.08%. Over the next seven trading days, the VIX surged 354% to 50.30% by February 6, 2018. The rise in VIX to just over 50% on that Tuesday was the single largest daily move in VIX in its history.

Following the rules, we covered all put positions that we wrote for the 7th, 9th, and 12th of February. Unfortunately, in those extreme environments, option prices escalate quickly and we were forced to cover the positions at a significantly higher price than they were sold for just a week earlier. Though painful, it is exactly these rules that prevent us from trying to predict where it’s going to stop and from turning our strategy to “hope”. We maximize the principal and live to write another day--when typically, richer premiums lend to us clawing back the losses relatively quickly.

We made the decision to pause writing calls based on our experience and market data. We have typically seen, even in a full-on correction, that the market can turn around quickly and have what our trader likes to call a “rip your face off rally.” We will continue to monitor the calls and plan to sell them strategically when attractive risk/reward opportunities arise.

Through a very peaceful 2017, we watched the premiums we were collecting for the put spreads decline significantly. The truth is that if the market never went against us, those premiums would eventually decline to nothing. Trading through the fastest, largest spike in VIX’s history was not fun, and we never want to lose any of our or our investors’ money. However, occasional losses are part of this strategy and when they occur, it tends to enhance the future economics of our strategy as the net premiums we receive rise and our strike prices are written more conservatively. In other words, the competition from other sellers is decreased and option buyers are willing to pay more as they regain a healthy fear.

Here are the composite net returns for the Portfolio Margin accounts for the periods indicated:

Reg. T Update

Here are the composite net returns for the Reg. T accounts for the periods indicated:

IRA accounts must use Reg. T Margin which, means that fewer option contracts can be written than in the “regular” accounts that use Portfolio Margin. Over time, this will result in lower returns when compared to the “regular” accounts.

HC Income Update

Here are the composite net returns for the HCP Income Strategy for the periods indicated:

Recap

February saw the Strategy post its most significant loss trading puts since August of 2015, on par with the losses incurred in 2011. A dramatic spike in volatility is the most challenging environment for the strategy and we went through the worst in VIX history in early February. As you may have inferred from our previous newsletters, we expected volatility to return at some point--we just couldn’t predict when or how fast. This strategy will take losses from time to time. If it didn’t, then no one would be paying us for the “insurance”. Try selling flood insurance in the Sahara. The rules we have in place are designed to help us trade through these environments without fear or greed and to come out the other end with good results.

The short VIX trade that made so many investors huge returns in 2017, turned and wiped many out. A historically “normal” move in volatility triggered the breakers in XIV and SVXY (two leveraged short VIX ETF’s) and caused them to flood the market with “cover” trades. These two funds alone amassed billions of dollars under management over the last couple years. That directional bet worked until it didn’t. This caused a bit of the tail wagging the dog, where the extreme move in VIX, coupled with the large decline in the S&P 500, resulted in us having to cover our positions.

This is a good time to remind our investors that we do not trade volatility. While it is obviously a factor in what we do, as volatility (VIX) is deduced from the price of options. We sell options on the S&P 500. We do not directly trade VIX.

About Horse Cove Partners LLC

Profiting from the art and science of taking risk.®

Horse Cove Partners was founded by Sam DeKinder and Kevin Ellis in January of 2013 with the commitment to help grow clients’ assets with a highly disciplined investment strategy, replicated weekly, to extract absolute returns from the market by trading short volatility option spreads. The firm was launched after more than two years of trading experience with personal assets that began in December of 2010. The firm is built on the strength of hedge fund trading expertise developed beginning in 2002.

Assets under management at the end of February 2018 were $124.7 million.

“We do not believe we are smarter than the market, nor can we time the market in any given week or month. As a result, we take an investment approach similar to an insurance company in that our investment strategy focuses on probability of success and the management of risk. We believe that it is possible to realize positive returns through disciplined focus on the risk of each trade with a weekly investment horizon, and accepting intelligent losses when risk events occur.”

We thank you for your continued support.

Sincerely,

Sam DeKinder, Kevin Ellis

Greg Brennan

Fiona Dyer

John Monahan

Michael Crissey

Don Trotter

sdekinder@horsecovepartners.com

kellis@horsecovepartners.com

gbrennan@horsecovepartners.com

fdyer@horsecovepartners.com

jmonahan@horsecovepartners.com

mcrissey@horsecovepartners.com

dtrotter@horsecovepartners.com

Horse Cove Partners LLC

1899 Powers Ferry RD SE

Suite 120

Atlanta, GA 30339

678-905-5723 main

1Net estimate on a consolidated basis of similar accounts as of 2.28.2018, which is preliminary and subject to revision. Performance estimate described herein as “YTD” are net of fees and expenses including a 2% per year management fee and 20% incentive fee and also assumes investors have been invested with no withdrawals.

This was prepared by Horse Cove Partners LLC a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Additional information about our firm is also available at www.adviserinfo.sec.gov. You can view the firm’s information on this website by searching by our firm name.

THIS MESSAGE AND ANY FILES TRANSMITTED WITH IT ARE CONFIDENTIAL AND PRIVILEGED. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE NOTIFY THE SENDER IMMEDIATELY AT 1 (678) 905-5723. IF YOU ARE NOT THE NAMED ADDRESSEE YOU SHOULD NOT COPY OR DISCLOSE THE CONTENT OF THIS MESSAGE AND OF ANY FILES TRANSMITTED WITH IT TO ANY OTHER PERSON.

Internet communications are not secure and subject to possible data corruption, either accidentally or on purpose, and may contain viruses. The content of this message should not be construed as an investment advice unless explicitly stated as such in the text of this message. Further, this message should not be construed as the solicitation of an offer to purchase or an offer to sell any securities or other financial instruments, including, without limitation, interest in any private investment managed by Horse Cove Partners LLC or any of its affiliated entities.

This material has been prepared solely for informational purposes only. Strategies shown are speculative, involve a high degree of risk and are designed for sophisticated investors.

Past performance is not a guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value. The information herein was obtained from third-party sources. Horse Cove does not guarantee the accuracy or completeness of such information provided by third parties. All information is given as of the date indicated and believed to be reliable. Performance results are estimates pending a verification. The returns are based on the Investment Manager's strategy and the compilation of actual client account trades. The Horse Cove Absolute Return and IRA Return strategies seek to extract absolute returns from the market by trading short volatility option spreads. The Enhanced Yield strategy seeks to achieve a targeted return trading only puts with a high probability of success.

The strategies reflect the deduction of advisory fees and any other expenses that a client would have paid or actually paid. The S&P 500 Index is used for comparative purposes only. The volatility of an index is materially different from that of the model portfolio. The S&P 500 refers to the Standard and Poor's 500 Index which is a capitalization-weighted index of 500 stocks. The index is designed to measure the performance of the broad domestic stock market. The VIX (CBOE volatility index) is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options. This volatility is meant to be forward looking and is calculated from both calls and puts. The VIX is a widely used measure of market risk and is often referred to as the "investor fear gauge." Investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown. Options trading entails a high level of risk. The models do not include the reinvestment of dividends and capital gains because options don't pay dividends. Please read the Characteristics and Risks of Standardized Options available from the Options Clearing Corporation website: http://www.optionsclearing.com for further details.

IRS CIRCULAR 230 NOTICE. Any advice expressed above as to tax matters was neither written nor intended by the sender or any Horse Cove Partners LLC affiliated entities to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed under U.S. tax law.