The month-end performance estimate as of January 31, 2015 for Horse Cove Partners Absolute Return Strategy is +4.70%, net of fees1. Since the inception of trading in December 2010, the strategy has achieved a total cumulative return of +173.69%.

Market Recap and Commentary

Is the top in? For the month of January, the S&P 500 Total Return Index fell (-3.00%). Since hitting a new all-time high on December 29, 2014 at 2093.55, the peak to trough so far, has been down -5.38%.

Not a good start for the markets in 2015. There is an old saying on Wall Street, “As January goes (specifically, the S&P), so goes the year.” According to the Stock Trader’s Almanac, since 1950, the January indicator has only five major errors for a 91.5% accuracy rate.

Volatility continued to run at levels consistently higher than we have seen in the past year, ranging from a low during the month of 15.52% and a high in mid-January of 23.43%. The average closing VIX was 19.12% which offered a good environment for selling options. As we mentioned in last month’s update, the average VIX in 2014, measured on a weekly closing basis, was 14.17%

There are a number of signs that the bull market, which has now run for 70 months, may be coming to an end, or may have ended in December. The average duration of a bull market since 1871 is 76 months, so it is likely that it will end sooner versus later.

For those of our readers who have significant investments in the “market” this is not good news. With the market down -3.0% for January, the S&P 500 now needs to return 17.75% in 11 months to equal last year’s performance. For comparison purposes, this is good news for the Horse Cove Partners Absolute Return Strategy because of its lack of correlation to the S&P 500.

Performance and Trading Update

With higher volatility, January proved to be a good month to be selling options. We had little margin pressure during the four trading weeks and benefited from the recapture of a mark-to-market loss carried over from December that resulted from the S&P 500 decline on Dec. 31 for options that expired on January 9.

The Horse Cove Partners Absolute Return Strategy has received its second consecutive Monthly Performance Award from BarclayHedge in the Option Volatility category for our December results. In a field of 17, we were ranked number 4 for the month of December.

We wrote puts and calls an average of 6.85% and 3.88% out of the money respectively. During the middle of the month, we wrote puts 8.4% out of the money when volatility was 22.87%. There was little margin pressure on our positions during the month.

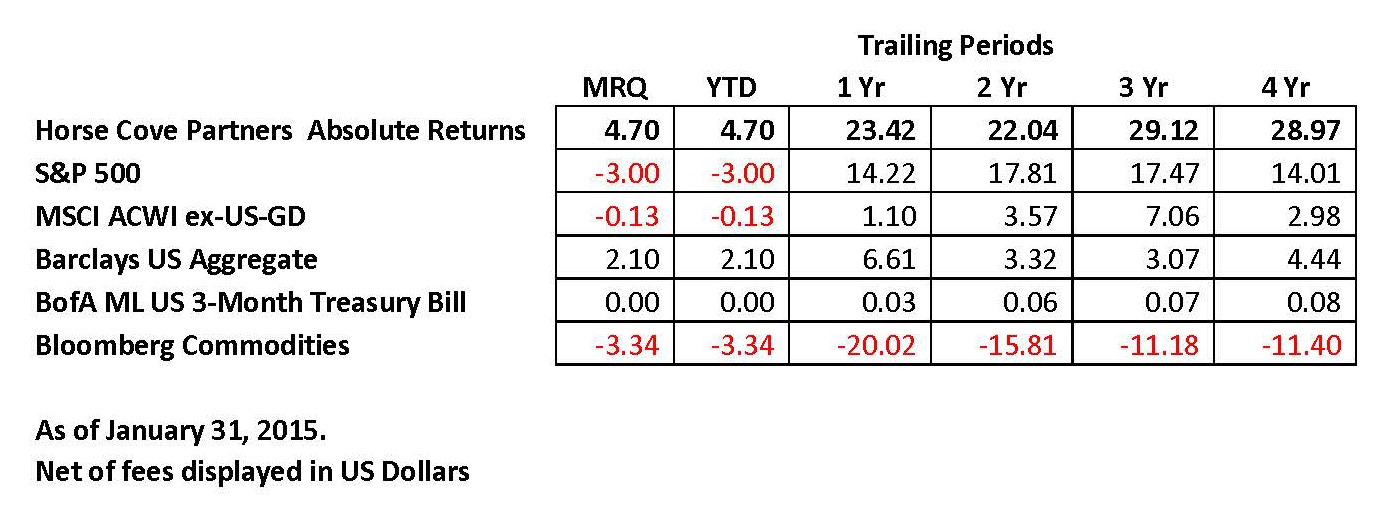

Here are the returns versus the S&P 500 total return index for the periods indicated:

IRA Update

Here are the returns for the consolidated IRA accounts for the periods indicated:

*Trading of IRA accounts began in September 2014. (1)

IRA accounts must use Reg. T Margin which means that fewer option contracts can be written than in the “regular” accounts that use Portfolio Margin. Over time, this will result in lower returns when compared to the “regular” accounts.

Goals of Every Investor

Every investor, advisor and consultant has two basic goals when it comes to investing that they are trying to achieve:

- Maintain or increase returns without increasing risk

- Lower risk and volatility without significantly lowering returns.

To accomplish those goals, diversification though portfolio allocation is a time-tested and well established practice. This is accomplished by adding asset classes that have a low or negative correlation to the existing asset allocations in the portfolio which can be expected to add incremental return. Prudent managers and investors alike strive to achieve these two major goals.

How does Horse Cove’s Absolute Return Strategy work to accomplish those two goals? Let’s look at returns first.

Here is a snapshot comparison to some other general asset classes:

Source: Evestment.com

Obviously, any portfolio with asset classes that have lower returns than those of Horse Cove, for the indicated period, would have benefited if an allocation had been made to the portfolio.

The second test is to look to see if the returns would come at a cost of adding risk and volatility to the portfolio. Standard deviation and drawdowns are two principle ways in which risk is measured. Since most portfolios contain equities (stocks), let’s compare Horse Cove’s results to the S&P 500, from the inception of trading, December 26, 2010 to January 31, 2015.

HC Partners S&P 500

Standard deviation: 11.29 10.42

Maximum Drawdowns -15.29% -19.82%

Recovery in months 3 5

Comparable standard deviation and maximum drawdowns.

Sources: www.stockcharts.com www.evestment.com

Last, there is little correlation of Horse Cove’s results to the S&P 500. The correlation coefficient is -.0216 to the S&P 500. [+1 is perfectly correlated, -1 is completely uncorrelated, 0 is randomly correlated to the S&P 500].

A small number of respected industry leaders such as Blackstone and Bill Gross are acknowledging the value of option volatility as another slice of the allocation pie. We couldn’t agree more as it meets by every measure, the major objectives to increase return and lower risk in a portfolio.

Horse Cove Update

We received an Award of Excellence from Barclay Hedge as the No. #4 in the Option Volatility category for December 2014.

With the addition, during the quarter, of one new account, the total assets under management now exceed $15.3 million in the Horse Cove Absolute Return strategy.

We value each of our clients and the assets each has entrusted to us in our strategy and will continue to pursue attractive returns to the benefit of all.

About Horse Cove Partners LLC

Profiting from the art and science of taking risk.®

Horse Cove Partners was founded by Sam DeKinder and Kevin Ellis in January of 2013 with the commitment to help grow clients’ assets with a highly disciplined investment strategy, replicated weekly, to extract absolute returns from the market by trading short volatility option spreads. The firm was launched after more than two years of trading experience with personal assets that began in December of 2010. The firm is built on the strength of hedge fund trading expertise developed beginning in 2002.

“We do not believe we are smarter than the market, nor can we time the market in any given week or month. As a result, we take an investment approach similar to an insurance company in that our investment strategy focuses on probability of success and the management of risk. We believe that it is possible to realize positive returns through disciplined focus on the risk of each trade with a weekly investment horizon, and accepting intelligent losses when risk events occur.”

We would like to thank you for your continued support and look forward to being in touch with you in the near future.

Sincerely,

Sam DeKinder, Kevin Ellis

John Monahan and Michael Crissey

sdekinder@horsecovepartners.com

kellis@horsecovepartners.com

jmonahan@horsecovepartners.com

mcrissey@horsecovepartners.com

Horse Cove Partners LLC

1899 Powers Ferry RD SE

Suite 120

Atlanta, GA 30339

678-905-5723 main

1Net estimate on a consolidated basis of similar accounts as of 1.31.2015, which is preliminary and subject to revision. Performance estimate described herein as “YTD” are net of fees and expenses including a 2% per year management fee and 20% incentive fee and also assumes investors have been invested with no withdrawals.

THIS MESSAGE AND ANY FILES TRANSMITTED WITH IT ARE CONFIDENTIAL AND PRIVILEGED. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE NOTIFY THE SENDER IMMEDIATELY AT 1 (978) 905 5723. IF YOU ARE NOT THE NAMED ADDRESSEE YOU SHOULD NOT COPY OR DISCLOSE THE CONTENT OF THIS MESSAGE AND OF ANY FILES TRANSMITTED WITH IT TO ANY OTHER PERSON.

Internet communications are not secure and subject to possible data corruption, either accidentally or on purpose, and may contain viruses. The content of this message should not be construed as an investment advice unless explicitly stated as such in the text of this message. Further, this message should not be construed as the solicitation of an offer to purchase or an offer to sell any securities or other financial instruments, including, without limitation, interest in any private investment managed by Horse Cove Partners LLC or any of its affiliated entities.

Finally, to the extent that performance information is contained in this message, you are hereby advised, and you acknowledge it, that past performance does not assure future results, which are not guaranteed by Horse Cove Partners LLC or any of its affiliated entities or by any insurance mechanism.

IRS CIRCULAR 230 NOTICE. Any advice expressed above as to tax matters was neither written nor intended by the sender or any Horse Cove Partners LLC affiliated entities to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed under U.S. tax law.